Research: Unpacking Nigeria’s agriculture opportunities

This article is based on a comprehensive research report on the investment opportunities in the agriculture sector of Nigeria. Executives and managers interested in the comprehensive report can approach Mr LIN Deyun at

dylin@ntu.edu.sg.

Growth in the urban population of Africa can potentially lead to a US$1tn regional market for African producers by 2030. Agriculture and food processing are vital for creating this $1tn industry.

Food processing is any intentional change in food occurring before consumption. Changing consumer demographics related to lifestyle changes, urbanisation, and tourism is resulting in an increased demand for convenience and processed foods. However, Africa’s agriculture and agribusiness industry is underperforming, providing opportunities for investors to benefit from this huge market.

The demand for convenience and processed food is growing in Nigeria. This demand is led by Nigeria’s expanding middle class, with consumer changes in tastes, patterns and style. Consumers are also becoming more health conscious, adding to the need for nutritious pre-packaged food. The food processing and packaging market report notes that Nigeria’s packaging and food processing market is one of the largest in Africa, estimated at about $545m. Between 2010 and 2012, imports of food processing and packaging technology increased 39%, from €198m ($236m) to €275m ($327m). The packaging industry experienced growth of 12% between 2010 and 2015.

The food processing and packaging market report also notes that the food and beverage industry accounts for 66% of total consumer expenditure, estimated at $150bn. It is the largest sector in manufacturing, accounting for 22.5% of the manufacturing industry. Small and medium enterprises account for 85% of companies, with 10% of total sales volume, while the big food and beverage players constitute 15%, with 90% of sales. In the packaged food sector, a 65% share of total revenue go to multinational firms who partner with local firms to repackage and market their products. The packaged foods sector has seen an influx of new players and products, making it one of the most dynamic sectors in the industry. Improved product quality and innovation, advertising and direct distribution all contribute to the dynamism.

- gaps-in-nigeria-demand-and-supply-300x311@2x.png (249.03 KiB) Viewed 4870 times

Nigeria’s agriculture and agribusiness industry is plagued with numerous challenges such as business, infrastructure and regulatory problems. Business challenges include the lack of funds, market share, cost of raw materials, taxation and other issues affecting the ease of doing business. There is inadequate infrastructure – such as power supply, transportation facilities and networks, and storage facilities – which can lead to a poor capacity for post-harvest handling, and high production and productivity costs. Regulatory challenges, such as insufficient food inspection, lack of standards and/or enforcement, hinder food processing and quality.

Food quality and safety systems need to be revamped to ensure the health of consumers and the competitiveness of food exports. There is a need for more food testing facilities, a strengthened inspectorate system and better co-ordination between federal agencies. Lessons from initiatives, such as the 2013-2018 European Union (EU)-funded National Quality Infrastructure Project for Nigeria (NQIP), should be put to good use. The NQIP, implemented by the United Nations Industrial Development Organisation, seeks to address challenges related to the quality of infrastructure, including providing trust for Nigerian products in regional and international markets, strengthening technical regulation and improving the enforcement of quality control of local and imported products.

The National Agency for Food and Drug Administration and Control (NAFDAC) and the Standards Organisation of Nigeria (SON) are beneficiaries of the NQIP, increasing the potential for policies and programmes to be implemented for food safety and improved industry regulations. A tangible outcome of the NQIP is the preparation of the National Directory of Testing and Calibration Laboratories in Nigeria. The directory featured 78 laboratories with a strong presence in Lagos, Port Harcourt and Abuja. It hopes to eventually cover the whole country and become a web tool accessible to all interested stakeholders. With regards to testing for foods, the directory lists a number of private and public laboratories. For instance, the SON’s directorate of laboratory services, which undergoes testing in its food technology laboratories in Lagos with sub-laboratories in microbiology, physio-chemical, micro-nutrients and mycotoxin, is involved in the testing of a number of food products listed in the directory. The directory is therefore a useful tool for companies who want to confirm the integrity, quality and competitiveness of their products in Nigeria.

Agricultural research is also necessary. The government needs to engage its numerous institutions to ensure the conduct of valuable, quality and accessible research that will increase productivity across the agricultural value chain. Nigeria’s National Agricultural Research system, made up of over 78 institutions and organisations, including research institutes, federal colleges of agriculture, agriculture facilities in universities and specialised agriculture universities, need to increase their efforts to engineer sustainable growth. Reasons cited for the failure to engineer growth include weak mechanisms for translating research into field usage and an inability to incentivise innovation. The private sector can help these institutions by more effectively collaborating with them in areas such as funding, professorships/chairs, scholarships and awards.

Despite the challenges, there is tremendous untapped potential in Nigeria’s agriculture and agribusiness sector. In the third quarter of 2016, the sector grew 4.88% and has grown by as much as 13% in previous years. The Nigerian government is prioritising agriculture with growth plans of 6.9% from 2017-2020. Rice, cashew nuts, groundnuts, cassava and vegetable oil are products the country hopes to export by 2020. There are plans to make Nigeria self-sufficient in tomato, rice and wheat by 2017, 2018 and 2019/2020 respectively. These goals will involve significant private sector investment and government collaboration and support.

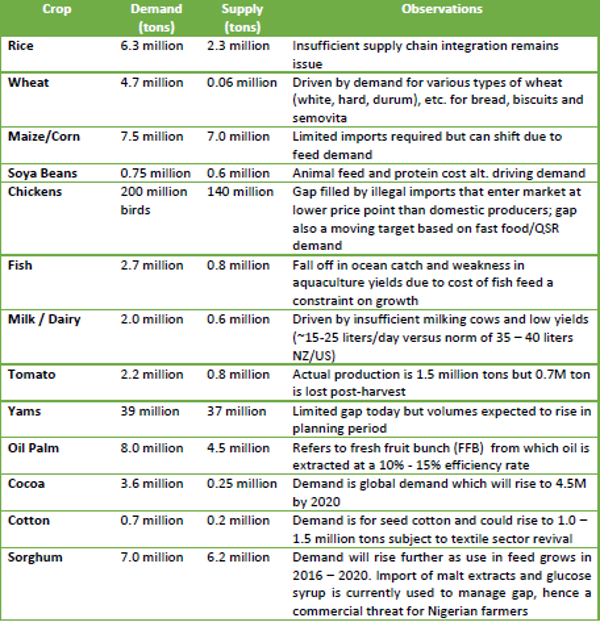

A broad range of food production and processing opportunities can be gleaned from The Green Alternative, Nigeria’s agriculture promotion policy document. It provides the following table with 2016 estimates of demand and supply gaps across key crops and activities in Nigeria.

The report focuses on the production and processing of nine core agriculture products. This includes four key crops on The Green Alternative list above – rice, tomato, chicken (poultry) and oil palm, as well as five other products – chicken eggs, fruit juice, mixed nuts (cashew and peanuts), cassava and organic fertilisers. The depth of research needed to cover all key crops listed in the green alternative necessitated a selection of key crops to be addressed.

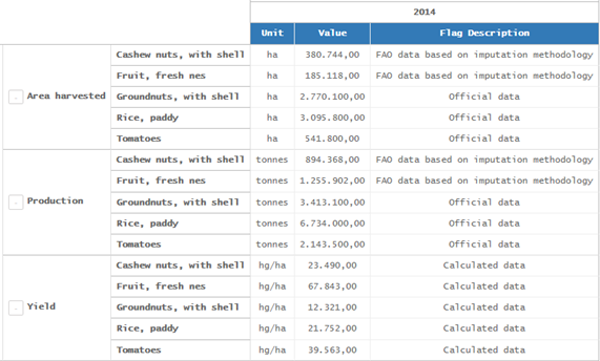

Statistics from the Food and Agriculture Organisation of the United Nations (FAO) on Nigeria’s 2014 production, yield and area harvested for rice, tomato, fruit, cashew and groundnuts, as well as chicken stocks, show Nigeria’s performance in the given year.

- Nigeria-food-stats-300x181@2x.png (95.81 KiB) Viewed 4870 times

Comparing selective sections of Nigeria’s 2014 agriculture performance with the statistics given for Western Africa below, Nigeria’s opportunities and capabilities in agriculture arguably are evident. For instance, Nigeria produced 2.1 million tonnes of tomatoes of the 3.5 million tonnes aggregate production for Western Africa.

The Green Alternative, FAO statistics and regional comparisons highlight the opportunities prevalent in Nigeria’s agribusiness sector. Focusing on the selected agricultural products in this report, there are investment opportunities for local production and strengthening processing capacities. This is more so considering the foreign exchange restrictions on the importation of rice, tomatoes, eggs, crude palm oil and poultry. The abundance of fruits, cashew and groundnuts, as well as the large consumer market, are also attractive for investors. Investors will be able to provide Nigeria with efficient productivity methods and value additions through processing, capable of taking Nigeria’s agribusiness to higher levels of growth and profitability.

Rice production is insufficient to meet the demand, and although there are a number of key players involved in backward integration and processing, more investment is needed in areas including land area, improving rice yields, training for small-farm holders, which make up more than 80% of farmers in the country, pre-milling and post-milling operations. The government’s plan to become self-sufficient as far as rice is concerned and ensuing initiatives to achieve this desire, should encourage private investment. Key players include the Olam Group, a Singapore global agribusiness company, the Dangote Group and the Bua Group, which are Nigerian entities.

Nigeria has the competitive advantage to lead worldwide tomato production. A major problem here is post-harvest loss. A number of initiatives, such as the Bank of Industry and Central Bank of Nigeria funds and interventions, YieldWise, GEMS4, which is linking farmers to processors, and other private sector solutions are making an impact. Investment opportunities in processing to make Nigeria self-sufficient in tomato paste and other tomato-based produce, are huge.

Chicken and egg production in Nigeria is set to grow to meet the increasing demand in protein-rich diets. The poultry sector is experiencing continued growth. However, there are investment opportunities in poultry equipment, breeding, feeding, milling and processing. The challenges caused by the high cost of poultry feed caused Olam to recently invest in animal feed mills, breeding farms, and a hatchery. Investments in the area of disease prevention, transport, logistics and processing are needed.

Opportunities for fruit production and processing go beyond the current key consumer preferences such as citrus, apple and mango. Investors may consider coconut, which can be processed into coconut water and coconut oil. The abundance of this fruit or nut in Nigeria, and the potential local and global demand for its beneficial value, makes it investment worthy. Nigeria’s fruit juice market, although maturing, has opportunities in the development of processing capacities. Inadequate production, post-harvest loss and lack of processing capacities still seem to be reasons for Nigeria’s continued importation of fruit juice concentrate. Dominant market players like Chi Limited are looking towards expanding the local sourcing of raw materials. The Nigerian agribusiness, Teragro, is investing in fruit production and processing, with the objective of reducing reliance on the importation of fruit concentrates.

Mixed nuts are gaining popularity in Nigeria’s domestic market, as well as globally. Nigeria’s comparative advantage in cashew and peanut production and the government’s plan to make cashew a foreign exchange cash crop, require investments. The mixed fruit sector also needs value adding processing capacities. Singapore companies may be interested in processing as Nigeria already exports some of its processed cashew to Singapore and other neighbouring Asian countries. The amount of cashew processed in Nigeria is minimal, with most of the produce being shipped to Vietnam, India and other intermediary countries for shelling, processing and packaging.

Cassava production and processing provide huge investment opportunities across the cassava value chain. Nigeria, the largest producer in cassava production, needs investments to improve yield and the area cultivated. Such investments include the acquisition of land, use of mechanised equipment and efficient farming technologies. The Bill and Melinda Gates Foundation is involved in a project to ensure the availability of certified quality seeds that have the potential to greatly increase yields. Investments are also needed to transform the lucrative cassava processing sector. There is huge unmet demand in the food sector for products such as high-quality cassava flour (HQCF), food-grade ethanol and starch, glucose and sweeteners. The use of HQCF for bread, if implemented successfully, will help reduce Nigeria’s wheat imports and further increase demand for cassava processing. Successful implementation would also require investments. Industrial starch for use in the pharmaceutical, paper, textile and adhesive industry and ethanol for biofuel, also provide huge potential.

Palm oil production in Nigeria needs investment to meet an increasing demand driven by household and industrial consumption. Nigeria, the top producer and exporter of palm oil in the 60s, is now a net importer. With over 90% of crude palm oil carried out by smallholder famers, there is room for investors to increase productivity. Okomu Oil and Presco, the largest commercial producers, account for just 7% of total crude palm oil production. This further highlights the need for more investments in the commercial production of palm oil. A number of companies, such as Dufil Prima Foods Plc and PZ Wilmar, are involved in backward integration with the potential to reap huge rewards.

Finally, Nigeria needs investments in the promotion and achievement of organic agriculture and fertiliser. Nigeria’s agricultural system, which mainly consists of smallholder farmers, is ideal for organic farming. Investments targeting farmer education and training, technical know-how, produce standards and organic fertiliser production would ensure participation in the $80bn global organic market and developing domestic market for organic fertiliser.

Conclusion

Nigeria’s potential for the agribusiness industry is good and largely untapped. The country’s large consumer market and huge population creates a real demand for food and food processing. This demand creates huge opportunities for investments. The availability of land, raw materials, affordable labour, and export potential also create investment opportunities. The Nigerian government’s increasing perception of the value in agriculture as a business and efforts to diversify the economy through agriculture, strengthen the agribusiness industry’s potential.

In particular, rice, tomato, poultry (chicken and eggs), oil palm, fruit juice, mixed nuts (cashew and peanuts), cassava and organic fertiliser are agriculture products that provide Nigeria with a comparative advantage. The government is partnering with the private sector to develop the value chain of these products. With private sector investments to boost local production and strengthen processing capacities, as well as government support and a business enabling environment, Nigeria’s agribusiness has the potential for increased growth levels and profitability.

Across the products examined in this report, investments pertaining to increasing land cultivation areas, improving yields, training for small farm holders, machinery and equipment, transport and logistics, storage, processing are needed. Processing and value add to products such as tomato, cassava, eggs, fruits and oil palm will positively impact Nigeria’s food security concerns, giving investors good returns. However, investors should be prepared to be involved in backward integration to guarantee supply of raw products for processing.

There is also the need to address the challenges hampering growth in the sector. Challenges such as constraints to land access, low levels of irrigation, limited agricultural research, high cost of farm inputs, availability and affordability of fertiliser, market access, post-harvest loss, infrastructure deficit and inadequate storage and processing facilities require investment and innovative ideas. While investors are beginning to participate actively in these areas, there is still room for more investors to come on board.

Private sector support in the form of import bans for products such as poultry, eggs (excluding hatching eggs) and fruit juice in retail packs and foreign exchange access for the importation of products such as rice, tomato, poultry (chicken and eggs) and palm kernel and palm oil products are incentives for investors to develop domestic production and manufacturing of agriculture products. Smuggling and corruption are vices that the government must deal with more effectively to truly incentivise investment and ensure domestic productivity.

Overall, investors should consider the opportunities and challenges present in the Nigerian agribusiness sector. Investors should further seek to convert challenges into opportunities. By investing in Nigeria’ agribusiness, specifically in areas with high growth potential and/or that the government has identified as priority for growth, the prudent investor has the best chance of reaping bountiful rewards.

The author, Dr Adefolake Adeyeye, is a Research Fellow of the NTU-SBF Centre for African Studies, a trilateral platform for government, business and academia to promote knowledge and expertise on Africa, established by the Nanyang Technological University and the Singapore Business Federation. Dr Adeyeye can be reached at

adefolake.adeyeye@ntu.edu.sg.